Munis weaker as investors digest larger supply, economic data, Fitch downgrade

5 min read

Municipals were weaker Wednesday as investors digested another larger new-issue slate, August redemption dollars, better-than expected economic data and the Fitch downgrade to the United States’ rating. U.S. Treasury yields rose slightly out long and equities sold off.

The weakness in munis and UST resulted partly from the ADP Employment Report that showed 324,000 jobs were added in July, well above the 175,000 forecast. That coupled with the Fitch of U.S. states.

Fundamentals are solid, “supported by the double-digit revenue growth that we saw over the last couple of years and has given states the ability to build up rainy day reserves,” South said.

States have done a good job budgeting for a potential slowdown, and then “if there are to be any shortfalls, they have these rainy day funds that can fill in any holes if they pop up,” she said.

Noble concurred, saying fundamentals are “fantastic,” with upgrades outstripping downgrades.

Muni-UST ratios are on the richer side, South noted.

The two-year muni-to-Treasury ratio Wednesday was at 63%, the three-year at 64%, the five-year at 65%, the 10-year at 65% and the 30-year at 87%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 63%, the three-year at 64%, the five-year at 64%, the 10-year at 66% and the 30-year at 89% at 4 p.m.

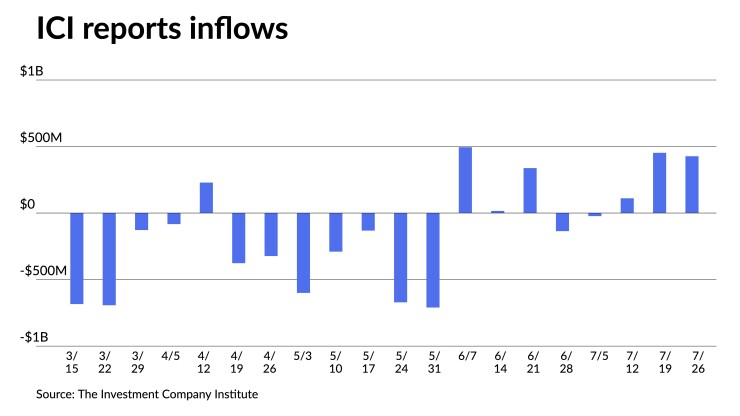

She said much of that has been driven by the technical environment within the muni market this year.

“The lack of supply within the market and stabilization of demand support the richer muni-UST ratios,” she said.

For the remainder of the year, munis will be rangebound, similar to where the asset class is now, Noble said.

Furthermore, he expects to see issuance tick up a little.

South said the muni market is in a “good spot as we go into the third quarter.”

Yields are a “little off of their highs of the year but still attractive, especially in a tax equivalent basis,” she said.

“Our overall view for the muni market is supportive and in a favorable outlook,” she said.

In the primary market Wednesday, J.P. Morgan preliminarily priced for institutions $1.654 billion of tax-exempt state sales tax revenue bonds, Series 2023A, from the Dormitory Authority of the State of New York (Aa1/AA+//), with yields cut up to nine basis points.

The first tranche, $1.339 million of Series 2023A-1, saw 5s of 3/2027 at 2.85% (unch), 5s of 2028 at 2.86% (+2), 5s of 2033 at 2.99% (+9), 5s of 2038 at 3.53% (+9), 4s of 2043 at 4.14% (+9), 4s of 2049 at 4.25% (+5) and 5s of 2053 at 4.07% (+8), callable 3/15/2033.

The second tranche, The second tranche, $314.900 million of Series 2023A-2, saw 5s of 23/2030 at 2.90% (+9) and 5s of 2033 at 2.99% (+9), callable 9/15/2029.

Barclays priced for San Antonio, Texas (Aa2/AA+/AA/), $288.830 million of water system junior lien revenue and refunding bonds, Series 2023A, with 5s of 5/2024 at 3.35%, 5s of 2028 at 3.02%, 5s of 2033 at 3.03%, 5s of 2038 at 3.48%, 5s of 2043 at 3.87%, 5.25s of 2048 at 4.04% and 4.375s of 2053 at par, callable 5/15/2033.

Wells Fargo priced for the Spring Branch Independent School District, Texas (Aaa/AAA//), $165.405 million of PSF-insured unlimited tax schoolhouse bonds, Series 2023, with 5s of 2/2025 at 3.31%, 5s of 2028 at 3%, 5s of 2033 at 3.06%, 5s of 2038 at 3.44%, 4s of 2043 at 4.24% and 4s of 2048 at 4.39%, callable 2/1/2033.

Secondary trading

California 5s of 2024 at 3.10%-3.08% versus 2.98%-2.94% on 7/10. Maryland 5s of 2024 at 3.31%-3.31%. NYC 5s of 2024 at 3.26%-3.24%.

Georgia 5s of 2028 at 2.77% versus 2.64% on 7/11. Connecticut 5s of 2028 at 2.88% versus 2.87% Tuesday. NYC TFA 5s of 2029 at 2.86%-2.84%.

Maryland 5s of 2032 at 2.60%. Washington 5s of 2033 at 2.79% versus 2.65% Friday and 2.63% original on Thursday. Board of Regents of the University of Texas System 5s of 2034 at 2.90%-2.92% versus 2.74% Thursday and 2.73% on 7/25.

Washington 5s of 2045 at 3.65%-3.67%. NYC TFA 5s of 2048 at 4.02%-4.03% versus 3.83%-3.81% on 7/21 and 3.84% original on 7/20. Metropolitan Water District of Southern California 5s of 2053 at 3.65% versus 3.55% Thursday and 3.61%-3.60% on 7/13.

AAA scales

Refinitiv MMD’s scale was cut six to seven basis points: The one-year was at 3.27% (+6) and 3.09% (+6) in two years. The five-year was at 2.76% (+6) , the 10-year at 2.67% (+6) and the 30-year at 3.61% (+7) at 3 p.m.

The ICE AAA yield curve was cut four to six basis points: 3.23% (+4) in 2024 and 3.11% (+5) in 2025. The five-year was at 2.73% (+6), the 10-year was at 2.65% (+6) and the 30-year was at 3.64% (+6) at 4 p.m.

The S&P Global Market Intelligence (formerly IHS Markit) municipal curve was cut six to seven basis points: 3.26% (+6) in 2024 and 3.09% (+6) in 2025. The five-year was at 2.76% (+6), the 10-year was at 2.67% (+6) and the 30-year yield was at 3.60% (+7), according to a 3 p.m. read.

Bloomberg BVAL was cut up seven basis points: 3.15% (+7) in 2024 and 3.04% (+7) in 2025. The five-year at 2.70% (+7), the 10-year at 2.63% (+7) and the 30-year at 3.62% (+7) at 4 p.m.

Treasuries were weaker out long.

The two-year UST was yielding 4.880% (-2), the three-year was at 4.546% (-2), the five-year at 4.229% (+1), the 10-year at 4.072% (+4), the 20-year at 4.356% (+5) and the 30-year Treasury was yielding 4.164% (+6) near the close.

Primary on Tuesday

Wells Fargo priced for the Long Island Power Authority, New York (A2/A/A/), $579.310 million of electric system general revenue bonds. The first tranche, $400 million of green bonds, Series 2023E, saw 5s of 9/2024 at 3.17%, 5s of 2028 at 2.87%, 5s of 2033 at 2.90%, 5s of 2038 at 3.41%, 5s of 2043 at 3.81%, 5s of 2048 at 4.02%, uninsured 5s of 2053 at 4.07% and Assured Guaranty-insured 5s of 2053 at 4%, callable 9/1/2033.

RBC Capital Markets priced for the Northwest Independent School District, Texas (Aaa//AAA/), $377.455 million of PSF-insured unlimited tax school building bonds, Series 2023, with 5s of 2/2024 at 3.34%, 5s of 2033 at 3.05%, 5s of 2038 at 3.44%, 4s of 2043 at 4.15%, 5s of 2048 at 4.01% and 4s of 2048 at 4.33%, callable 2/15/2032.

Primary to come

The Crowley Independent School District, Texas, (Aaa//AAA/) is set to price Thursday $425.775 million of PSF-insured unlimited tax school building bonds, Series 2023, serials 2024-2043, terms 2048, 2053. Siebert Williams Shank & Co.

The Texas Private Activity Bond Surface Transportation Corp. is set to price Thursday on behalf of the North Tarrant Express Mobility Partners’ North Tarrant Express project $406.540 million of senior lien revenue bonds, Series 2023. J.P. Morgan Securities.

The Oklahoma Water Resources Board (/AAA//) is set to price Tuesday $176.805 million of state loan program revenue bonds, Series 2023B, serials 2024-2038, terms 2043, 2048, 2053. BOK Financial Securities.

The Birdville Independent School District, Texas, (/AAA/AAA/) is set to price Thursday $145.985 million of PSF-insured unlimited tax school building bonds, Series 2023-A. FHN Financial Capital Markets.

The Pennsylvania Economic Development Financing Authority (//BBB+/) is set to price Thursday $128.850 million of Presbyterian senior living refunding revenue bonds, consisting of $35.180 million of Series 2023B-1 and $93.670 million of Series 2023B-2. Piper Sandler & Co.

The Nebraska Investment Finance Authority (/AAA//) is set to price $109.630 million of single-family housing revenue bonds, consisting of non-AMT social bonds, Series 2023E, and taxables, Series 2023F. J.P. Morgan Securities.