Munis mixed amid UST volatility; 10-year UST hits high not seen since 2008

6 min read

Municipals were mixed Wednesday amid another busy new-issue day led by the University of California Regents in the negotiated space and gilt-edged Tennessee in the competitive market. U.S. Treasuries were weaker again, pushing the 10-year UST to a high not seen since 2008. Equities ended the trading session down.

Triple-A benchmarks saw cuts out long, but saw strength on the short end, while U.S. Treasury yields rose four to five basis points with the 10-year eclipsing 4.25%.

Muni to UST ratios reacted accordingly. The two-year muni-to-Treasury ratio Wednesday fell to 62%, the three-year at 63%, the five-year at 63%, the 10-year at 65% and the 30-year at 86%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 63%, the three-year at 64%, the five-year at 63%, the 10-year at 65% and the 30-year at 86% at 4 p.m.

With the overhang of a volatile U.S. Treasury market, municipals are seeing an interesting dynamic, said Jeff Timlin, a managing partner at Sage Advisory.

“There’s strength in the market, a lot of buying, a lot of interest, yet we’re seeing a little bit of a sell off here, at least on rates,” he said. “But that’s primarily driven by the direction of Treasury rates.”

Spreads, he said, have compressed rather substantially over the past several weeks.

There have been some adjustments across the board in various sectors and states, but holistically, he said there seems to be interest for munis.

The readjusted yield levels have kept the market fairly well bid, according to Timlin.

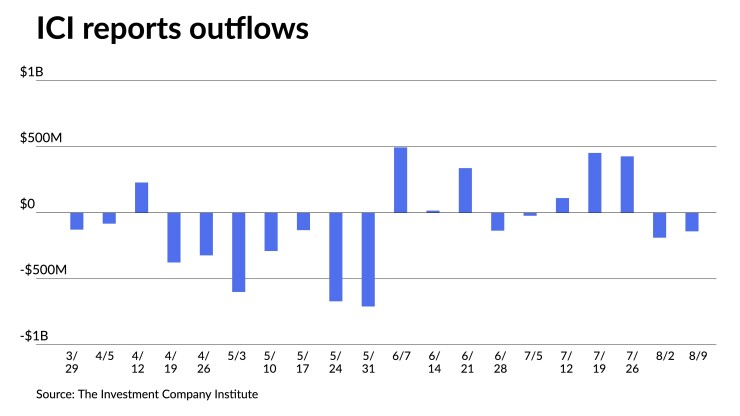

“There’s been a shift in terms of the dynamic of the market, and mutual funds have continued to see outflows while [exchange-traded funds] and [separately managed accounts] funds have seen inflows, and that’s what’s kept the support in the marketplace,” he said.

The Investment Company Institute reported investors pulled $141 million from municipal bond mutual funds in the week ending Aug. 9, after $187 million of outflows the previous week. ETFs saw inflows of $550 million after $533 billion of outflows the week prior.

Summertime sees “ebbs and flows of illiquidity, and by that, it just means larger bid-ask spreads in the market,” he said.

However, Timlin said that is temporary, due in part to participants being on vacation in the summer months, which is coming to an end.

Issuance is decent despite being down 16.1% through the end of July year-over-year, according to Refinitiv data.

“That has led to some support to the environment in terms of not flooding the market with too much paper,” he said.

There has been an influx of Texas paper, which includes several large Texas school districts’ deals over the past several weeks. This has caused Texas spreads to widen substantially in the 40 basis point to 50 basis point range on selective deals.

There have been disjointed markets and mispricings “here and there,” but he noted that’s typical of the summer months and periods where not all participants are paying attention.

Technicals are still very strong, but he said that should be lessening.

“We’re in that last month of the seasonal demand period, with $35 billion in terms of maturity and coupon payments ” that came due on Aug. 1 and 15, he said.

That money is being reinvested, with there being a “pretty significant rally” in California and New York paper since the beginning of the month, along with several other triple-A-rated states.

These states, he said, were not big issuers during the summer months.

From an individual state perspective, there was a large net negative supply dynamic in certain states, he noted. Investors are forced to buy richer paper in specialty states to keep their allocation aligned with the index they are running against, he noted.

Timlin expects the supply-demand imbalance to be persistent.

Many firms revised their issuance forecast for the year downward in their mid-year reports.

“With rates higher, rates are going to be a major driver of what’s going to happen,” he said.

He expects issuance to be down 30% year-over-year, but if rates decline there could be a smaller figure as more refunding deals come to market. With rates this high, he said “refunding deals come off the table.”

Furthermore, new issuance can sometimes be constrained “because when issuers were used to 1% levels, and now they’re at 3%, maybe sometimes 4% level, they might feel a little gun shy in coming to market to fund certain projects if they don’t have to or if it’s on the margin,” he said.

That dynamic will continue to be in place, and demand should remain relatively stable, which will be supportive for the market, according to Timlin.

“The magnitude of that negative supply in terms of how it got exacerbated in the summer because of all the money that was coming due from maturity coupon payments will lessen,” he said.

From now through the end of the year, he said there will be a “bias” toward not enough supply coming to market to satiate all the demand that is out there.

In the primary market Wednesday, Siebert Williams Shank priced for the Regents of the University of California (Aa2/AA/AA/) $706.595 million of general revenue bonds. The first tranche, $586.545 million of tax-exempts, 2023 Series BQ, with 5s of 5/2029 at 2.73%, 5s of 2033 at 2.75% and 5s of 2035 at 2.94%, callable 5/15/2033.

The second tranche, $120.050 million of taxables, 2023 Series BR, saw 5.1s of 5/2033 price at par.

Barclays priced for Chicago (/AA//) $171.970 million of Chicago O’Hare International Airport customer facility charge senior lien refunding bonds, Series 2023, with 5s of 1/2028 at 3.39%, 5s of 2033 at 3.54%, 5s of 2038 at 4.04% and 5.25s of 2043 at 4.24%, callable 1/1/2033.

In the competitive market, Tennessee (Aaa/AAA/AAA/) sold $449.420 million of GOs, Series 2023A, to Wells Fargo Bank, with 5s of 5/2024 at 3.25%, 5s of 2029 at 2.92%, 5s of 2033 at 2.95%, 5s of 2038 at 3.55% and 5s of 2043 at 3.83%, callable 5/1/2033.

Muni CUSIP requests fall

Municipal CUSIP request volume decreased in July on a year-over-year basis, following an increase in June, according to CUSIP Global Services.

For muni bonds specifically, there was a decrease of 26.2% month-over-month and an 18.6% decrease year-over-year.

The aggregate total of identifier requests for new municipal securities, including municipal bonds, long-term and short-term notes, and commercial paper, fell 30.2% versus June totals. On a year-over-year basis, overall municipal volumes were down 15.9 %. CUSIP requests are an indicator of future issuance.

Secondary trading

NYC 5s of 2024 at 3.22%-3.17% versus 3.25% Tuesday and 3.24% Monday. Massachusetts 5s of 2024 at 3.22%. Triborough Bridge and Tunnel Authority 5s of 2024 at 3.17%.

Louisiana 5s of 2028 at 2.99%. DC 5s of 2028 at 2.77% versus 2.80% on 8/10 and 2.85%-2.81% on 8/8. Ohio 5s of 2029 at 2.84%-2.81%.

Virginia 5s of 2032 at 2.69%-2.68%. Harris County, Texas, 5s of 2035 at 3.28% versus 3.27% original on 8/9. DASNY 5s of 2036 at 3.37%-3.36% versus 3.38% original on 8/3.

Washington 5s of 2048 at 4.06%-4.05% versus 3.98% Friday. NYC 5s of 2048 at 4.14% versus 4.17% Tuesday and 4.16%-4.13% Monday. Massachusetts 5s of 2053 at 4.11% versus 4.02%-4.00% on 8/10 and 4.02%-4.00% on 8/9.

AAA scales

Refinitiv MMD’s scale saw cuts out long: The one-year was at 3.20% (-2) and 3.10% (unch) in two years. The five-year was at 2.77% (unch), the 10-year at 2.75% (unch) and the 30-year at 3.73% (+2) at 3 p.m.

The ICE AAA yield curve saw cuts 10 years and out: 3.21% (-4) in 2024 and 3.13% (-1) in 2025. The five-year was at 2.77% (unch), the 10-year was at 2.72% (+1) and the 30-year was at 3.73% (+2) at 4 p.m.

The S&P Global Market Intelligence (formerly IHS Markit) municipal curve was cut out long: 3.21% (-2) in 2024 and 3.10% (unch) in 2025. The five-year was at 2.78% (unch), the 10-year was at 2.76% (unch) and the 30-year yield was at 3.72% (+2), according to a 4 p.m. read.

Bloomberg BVAL was cut up to two basis points: 3.19% (unch) in 2024 and 3.09% (unch) in 2025. The five-year at 2.77% (unch), the 10-year at 2.73% (+1) and the 30-year at 3.73% (+2) at 4 p.m.

Treasuries were weaker.

The two-year UST was yielding 4.978% (+4), the three-year was at 4.682% (+5), the five-year at 4.416% (+5), the 10-year at 4.264% (+2), the 20-year at 4.547% (+5) and the 30-year Treasury was yielding 4.362% (+4) at the close.

Primary to come

The Los Angeles Unified School District (A2//A-/) is set to price Thursday $384.260 million of certificates of participation, sustainability bonds, Series 2023A, serials 2024-2038. BofA Securities.

The Dormitory Authority of the State of New York (Aa2//AA/) is set to price Thursday $300 million of New York and Presbyterian Hospital Obligated Group revenue bonds, Series 2023A. Goldman Sachs.