August issuance falls 13%

4 min read

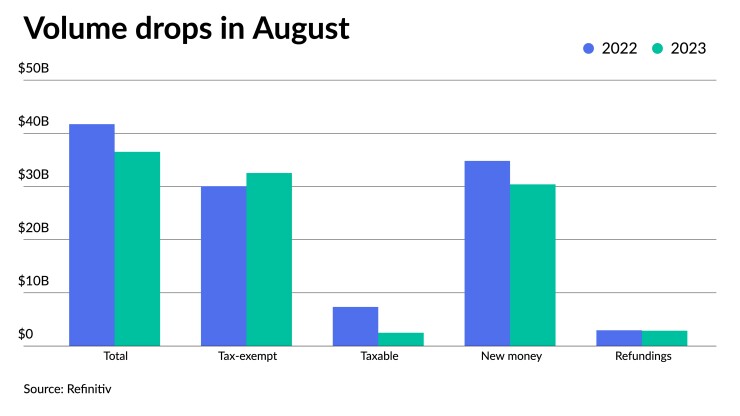

August municipal bond issuance fell 13% from 2022 as some issuers were less inclined to price deals amid continued market volatility and rising interest rates. Despite this, August saw the largest monthly volume of 2023, helped by several billion-dollar deals and multiple Texas school district deals.

August’s total volume was $36.514 billion in 728 issues, down from $41.716 billion in 751 issues a year earlier, and lower than the $38.101 billion 10-year average, according to Refinitiv data.

Total issuance through Thursday is at $244.677 billion, down 15.1% from $288.204 billion through the same timeframe in 2022.

Tax-exempt issuance rose 8.2% to $32.533 billion in 664 issues from $30.058 billion in 669 issues in 2022. Taxable issuance totaled $2.502 billion in 55 issues, down 66% from $7.358 billion in 68 issues a year ago. Alternative-minimum tax issuance dropped to $1.479 billion, down 65.6% from $4.300 billion.

New-money issuance fell 12.7% to $30.401 billion from $34.812 billion a year prior. Refunding volume fell 2.8% to $2.886 billion from $2.968 billion in 2022.

“Issuance followed a very familiar trajectory in August, given unrelenting market volatility that essentially catalyzed a bond market sell-off surrounding the looming Jackson Hole Economic Symposium as well as a growing tone of higher for longer,” said Jeff Lipton, managing director of credit research at Oppenheimer Inc.

Unlike last year, there was more of a fixation on Fed Chairman Jerome Powell’s speech at Jackson Hole, he noted.

For much of this year, there has been hesitation from the issuer community “fixated on the vagueness of monetary policy,” he said.

Issuers that “had critical funding needs and/or a desire to fulfill existing bond authorizations were more compelled to access the market for new-money purposes,” but new-money issuance for August is still down year-over-year, Lipton said.

At this time last year, the Fed’s tightening campaign was well underway with 225 basis points of rate hikes “already down on the books,” with more expected to come, he said.

At that time, refunding opportunities were “losing economic viability, and with rates higher today, the universe of refunding candidates has dried up considerably,” Lipton said. Refundings only dropped slightly year-over-year in August but more significant decreases can be seen in previous months.

“One is that issues that held supply back in 2022 was thinking that raising rates is going to be temporary, [and they] came into 2023, possibly realizing that rates are here to stay,” said Eve Lando, portfolio manager and managing director at Thornburg Investment Management.

Currently, Lipton said, there is an 11% to 12% of a 25 basis point rate hike at the September Federal Open Market Committee meeting following Powell’s speech at Jackson Hole and the release of “more market-friendly data points.” And if there is more market-friendly data on Friday, he said that probability should move lower.

Moreover, states and local governments are still flushed “COVID money,” Lando said.

“Things have been rather positive for states and local governments, and there hasn’t been a lot of need to issue [but rather] deal with things that could wait,” she said.

The “available pandemic generated stimulus that has given many issuer types some financial cushion and that lessens the need for debt financing,” Lipton said.

However, he noted, “much of this funding has been spent down, along with more challenged revenue and budgetary backdrops, certain issuers will find themselves hard pressed to avoid the capital markets.”

“So through the balance of the year, rates, and the outlook for rates will certainly drive supply,” he said. “Should the most hawkish scenarios unfold, issuers may capitulate and be grudgingly take on higher levels of debt to lock in what is perceived to be better financing term.”

However, he doesn’t believe the most hawkish scenario will take place and there is room for rates to stabilize, if not dip lower.

But while some issuers were hesitant to come to market, August saw several billion-dollar deals from issuers, including a $1.2 billion Michigan Trunkline deal and a $1 billion New York City Transitional Finance Authority deal.

“We did have some visibly large deals, which to a certain extent likely skewed the August issuance figures,” Lipton said.

Part of that has to do with “certain issuers wanting to access the capital markets before what is perceived to be higher borrowing costs,” he said.

Additionally, the influx of PSF-backed Texas school deals played a role

Every week has seen several school districts “taking advantage or getting it in front before things change with PSF provisions, and just issuing in large numbers,” Lando said.

At the beginning of the month, she said the PSF-backed Texas school deals priced well, but as August progressed, things got cheaper.

“So that was to highlight a really good opportunity in buying of something that’s so high quality as a triple-A PSF school district paper,” she said.

Issuance details

Revenue bond issuance decreased 24.4% to $21.543 billion from $28.486 billion in August 2022, and general obligation bond sales rose 13.2% to $14.971 billion from $13.230 billion in 2022.

Negotiated deal volume was down 6.2% to $29.948 billion from $31.913 billion a year prior. Competitive sales decreased 6.2% to $6.288 billion from $6.705 billion in 2022.

Deals wrapped by bond insurance were at $2.648 billion in 132 deals from $1.821 billion in 116 deals in 2022, a 45.4% increase.

Bank-qualified issuance rose 4.2% to $855.3 million in 219 deals from $820.7 million in 192 deals a year prior.

In the states, Texas claimed the top spot year-to-date.

Issuers in the Lone Star State accounted for $46.529 billion, up 28.7% year-over-year. California was second with $34.103 billion, up 2.5%. New York was third with $24.996 billion, down 32.6%, followed by Illinois in fourth with $8.648 billion, down 10.5%, and Florida in fifth with $8.243 billion, a 35.9% decrease from 2022.

Rounding out the top 10: Michigan with $6.619 billion, down 19.4%; Washington with $6.355 billion, down 18.1%; Georgia with $6.346 billion, down 19.6%; Wisconsin at $5.995 billion, down 1.3%; and Pennsylvania with $5.410 billion, down 21.4%.