Munis steady ahead of smaller new-issue calendar

6 min read

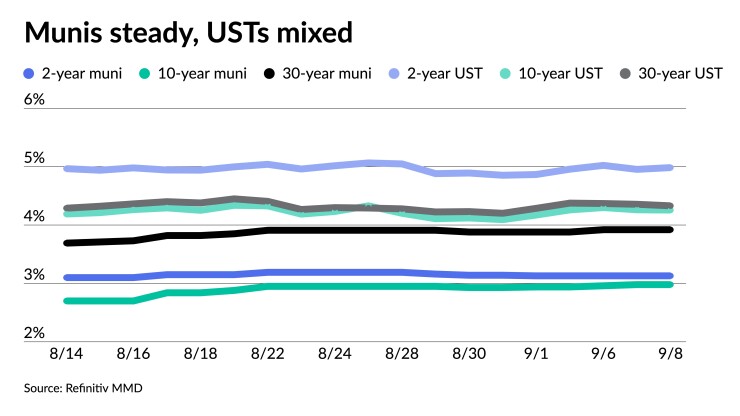

Municipals were steady Friday ahead of a smaller new-issue calendar. U.S. Treasuries and equities ended mixed.

The two-year muni-to-Treasury ratio Friday was at 63%, the three-year was at 64%, the five-year at 65%, the 10-year at 70% and the 30-year at 90%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 64%, the three-year at 65%, the five-year at 65%, the 10-year at 69% and the 30-year at 90% at 4 p.m.

USTs reached multi-year highs in the middle of August, but “yields declined meaningfully by the end of the month, before reversing their course in response to stronger economic data,” Barclays strategists said.

Historically, “September and, to a lesser degree, October have not been kind to municipal investors,” they said.

The last time investors saw “sizable” returns in the fall was 2015, they noted.

Over the past 10 years, returns for September have averaged negative 0.3%, while October returns have been “near zero.” Over the past five years, returns have been negative 5.7% and negative 1.8%, respectively.

The Barclays strategists said they were “cautious going into August (and the IG and HY tax-exempt municipal indices each lost about 1.5% last month), but [they] are much less negative for this month.”

“While MMD-USD ratios have adjusted slightly lower in early September, they ended August at relatively attractive levels: 72% for 10y and 92% for 30y, the highest levels since March, making current levels much more attractive than earlier this summer,” they said.

However, the strategists noted, there has been an uptick in supply, with August seeing the heaviest monthly issuance year-to-date. This, they said, was likely responsible for recent muni underperformance.

Supply in September is “also slated to be robust, but might not be as heavy as last month, as the 30-day visible supply pipeline does not look overwhelming,” they said. The Bond Buyer 30-day visible supply is at $9.35 billion.

Meanwhile, they said, “muni bond redemptions will dip by a large margin, leaving less money in investor hands.”

In September, they expect $20 billion of bond redemptions and $7 billion in coupon payments. California, New York and Texas will see the lowest expected net supply, they said.

Additionally, fund flows will remain “anemic,” they said. This week saw sizable outflows as investors pulled $798 million from muni mutual funds, according to Refinitv Lipper.

Overall, they said, “it is hard to be overly optimistic about municipals this month, and rate volatility will also likely persist, while T-bills yield close to 5.5%, making other investment alternatives much less attractive.”

Barclays strategists view range-bound trading as the most likely outcome this month.

Therefore, they said, the best strategy is “to add only on weakness versus Treasuries, while also trimming exposure when munis outperform.”

Overall, Barclays strategists said, “unless the muni market sells off meaningfully, investors should remain relatively light going into October.”

New-issue calendar

The calendar will fall, with an estimated $2.645 billion expected the week of Sept. 11, with $1.244 billion of negotiated deals on tap and $1.401 billion on the competitive calendar.

The Central Plains Energy Project leads the negotiated calendar with $621 million of gas project revenue refunding bonds, followed by $437 million of general receipt bonds from Ohio State University and $372 million of airport revenue bonds from Charlotte, North Carolina.

The competitive calendar is led by Montgomery County, Maryland, with $280 million of consolidated public improvement bonds, followed by $185 million of GOs from the Las Vegas Valley Water District and $166 million of GOs from the Greenville County School District, South Carolina.

Secondary trading

Georgia 5s of 2024 at 3.28% versus 3.26% Tuesday and 3.28% on 8/28. Minnesota 5s of 2024 at 3.36%. Washington 5s of 2025 at 3.27%-3.25%.

DASNY 5s of 2027 at 3.12%. Maryland 5s of 2029 at 2.94%. California 5s of 2030 at 3.06%.

Oregon 5s of 2032 at 3.05%. Mecklenburg, North Carolina, 5s of 2034 at 3.05% versus 2.98% on 8/29. Indiana Finance Authority 5s of 2035 at 3.25%-3.24% versus 3.16% Wednesday and 3.21%-3.20% on 8/30.

Massachusetts 5s of 2047 at 4.11%. Washington 5s of 2048 at 4.19%. NYC 5s of 2051 at 4.40%-4.38% versus 4.42%-4.37% Thursday and 4.30%-4.29% Tuesday.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 3.25% and 3.13% in two years. The five-year was at 2.88%, the 10-year at 2.98% and the 30-year at 3.92% at 3 p.m.

The ICE AAA yield curve was bumped up to a basis point: 3.26% (unch) in 2024 and 3.18% (unch) in 2025. The five-year was at 2.90% (unch), the 10-year was at 2.94% (unch) and the 30-year was at 3.93% (-1) at 4 p.m.

The S&P Global Market Intelligence (formerly IHS Markit) municipal curve was unchanged: 3.26% in 2024 and 3.14% in 2025. The five-year was at 2.89%, the 10-year was at 2.98% and the 30-year yield was at 3.91%, according to a 3 p.m. read.

Bloomberg BVAL was little changed: 3.25% (unch) in 2024 and 3.16% (unch) in 2025. The five-year at 2.88% (unch), the 10-year at 2.89% (unch) and the 30-year at 3.89% (unch) at 4 p.m.

Treasuries were mixed.

The two-year UST was yielding 4.983% (+3), the three-year was at 4.690% (+2), the five-year at 4.395% (flat), the 10-year at 4.256% (-1), the 20-year at 4.522% (-2) and the 30-year Treasury was yielding 4.329% (-3) near the close.

Primary on Thursday

Citigroup Global Markets priced and repriced $2.582 billion of various purpose GOs for California (Aa2/AA-/AA/), with yields cut from Wednesday’s retail offering and then cut further from Thursday’s preliminary pricing.

The first tranche, $1.045 billion of new money bonds, saw 5s of 9/2026 at 3.08% (+5), 5s of 2033 at 3.11% (+4), 5s of 2038 at 3.61% (+4) and 5.25s of 2053 at 4.11% (+3), callable 9/1/2033.

The second tranche, $1.536 billion of refunding bonds, saw 5s of 9/2024 at 3.23% (unch), 5s of 2028 at 3.03% (+5), 5s of 2032 at 3.08% (+5), 4s of 2043 at 4.17% (+2) and 5s of 2043 at 3.89% (+4), callable 9/1/2033.

Primary to come

Central Plains Energy Project (Aa2///) is set to price $621.255 million of Project No. 4 taxable gas project revenue refunding bonds. Goldman Sachs.

Ohio State University (Aa1/AA/AA+/) is set to price Tuesday $437.465 million of multiyear debt issuance program II general receipt bonds, consisting of $267.270 million of green new-issue bonds, Series B, serials 2024-2033 and 2035; and $170.195 million of refunding bonds, Series C, serials 2046 and 2056. RBC Capital Markets.

The university (/AAA/AA+/) is also set to price $258.780 million of multiyear debt issuance program II term variable rate general receipts refunding bonds, consisting of $117.630 million of Series D-1, term 2035, and $141.150 million of Series D-2, term 2044. RBC Capital Markets.

Charlotte (Aa3//AA-/) is set to price Thursday $372.115 million of Charlotte Douglas International Airport revenue bonds, consisting of $260.175 million of non-AMT bonds, Series 2023A, serials 2025-2043, terms 2048 and 2053, and $111.940 million of AMT bonds, Series 2023B, serials 2025-2043, terms 2048 and 2053. BofA Securities.

The California Health Facilities Financing Authority (Aa3/AA-/AA/) is set to price Tuesday $261.5 million of Stanford Health Care revenue bonds, Series 2023A. Morgan Stanley & Co.

Austin (/AAA/AA+/) is set to price Tuesday $257.425 million, consisting of $222.825 million of public improvement and refunding bonds, serials 2024-2043; $25.830 million of certificates of obligation, serials 2024-2043; and $8.770 million of public property finance contractual obligations, serials 2024-2030. RBC Capital Markets.

Honolulu (/AA+/AA/) is set to price Wednesday $188.835 million of senior green wastewater system revenue bonds, serials 2028-2043, terms 2048 and 2053. BofA Securities.

The Arlington County Industrial Development Authority, Virginia, (/A+/AA-/) is set to price Tuesday $150 million of revenue bonds. J.P. Morgan Securities.

The Ohio Water Development Authority (Aaa/AAA//) is set to price Thursday $150 million of Ohio Drinking Water Assistance Fund sustainability revenue bonds, Series 2023A. Jefferies.

The Oregon House and Community Services Department (Aa2///) is set to price Tuesday $147.665 million of single-family mortgage program mortgage revenue bonds, consisting of taxable 2023 Series C bonds, and non-AMT 2023 Series D bonds. J.P. Morgan Securities.

The Indiana Public Schools Multi-School Building Corp. (/AA+//) is set to price Wednesday $127.040 million of unlimited ad valorem property tax first mortgage social bonds, serials 2024 and 2029-2043, insured by Indiana State Aid Intercept Program. Stifel, Nicolaus & Co.

Grand Forks, North Dakota, (Baa3//BBB-/) is set to price Tuesday $126.680 million of Altru Health System revenue bonds, serials 2026-2043, terms 2048 and 2053. BofA Securities.

The Colorado Regional Transportation District (Aa2/AAA//) is set to price Tuesday $113.780 million of FasTracks Project sales tax revenue refunding bonds, Series 2023A. Jefferies.

The Arlington Higher Education Finance Corp., Texas, (/AAA//) is slated to price $107.360 million of Trinity Basin Preparatory education revenue bonds, serials 2025-2043, terms 2048 and 2053, insured by the Texas Permanent School Fund Guarantee Program. RBC Capital Markets.

Competitive

Greenville County School District, South Carolina, is set to sell $166.350 million of GO bonds, Series 2023B at 11 a.m. eastern Tuesday.

Minneapolis is set to sell $114.925 million of GO bonds at 11 a.m. Tuesday.

The Las Vegas Valley Water District (Aa1/AA//) is set to sell $184.830 million of general obligation limited tax water bonds at 10:45 a.m. eastern Wednesday.

Montgomery County, Maryland, is set to sell $280 million of consolidated public improvement bonds, Series 2023A, at 10 a.m. eastern Thursday.

Wichita, Kansas, is set to sell $113.875 million of GO temporary notes at 10:30 a.m. Thursday.

Christine Albano contributed to this story.