Munis steady as Connecticut prices for retail

4 min read

Municipals were little changed Monday as U.S. Treasuries were weaker and equities ended up.

Volume this week is relatively light with the new-issue calendar estimated at $1.6 billion. There are only two deals over $100 million.

The Bond Buyer 30-day visible supply sits at $4.03 billion.

In the primary market Monday, Jefferies held a one-day retail order for $826.340 million of

The second tranche, $250 million of social GOs, 2024 Series B, saw 5s of 1/2037 at 2.94%, 5s of 2038 at 3.06%, 4s of 2043 at 3.74% and 5s of 2044 at 3.46%, callable 1/15/2034.

The third tranche, $176.340 million of social refunding GOs, 2024 Series C, saw 5s of 1/2025 at 2.66%, 5s of 2028 at 2.45%, 5s of 2033 at 2.51% and 5s of 2034 at 2.53%, noncall.

For most of last week, muni participants “largely sat on the sideline until after the Fed meeting, with multiple dealers citing a lack of depth amidst unattractive valuations,” Birch Creek Capital strategists said in a report.

“Accounts were looking to hide out through year-end and were only willing to put money to work if they could source bonds 10bp+ behind the offered side,” they said.

Bid wanteds were “sparse” and sellers were “only looking to hit bids where they could get levels close to what appeared to be rich and stale evals,” Birch Creek strategists said.

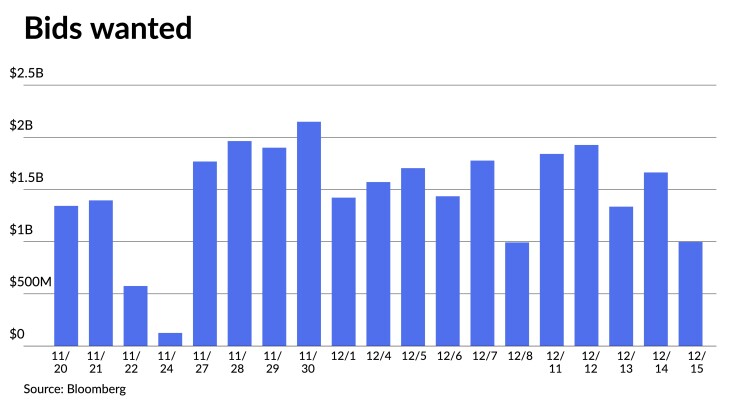

Clients put up about $7.76 billion up for the bid with Tuesday having the most volume of bids-wanted at $1.93 billion, according to Bloomberg.

All that changed after digesting Wednesday’s monumental Fed pivot, they said.

The AAA Refinitiv MMD curve rallied 17 basis points on Thursday, “its best day of performance in over three years and continued to see yields fall on Friday,” they noted.

“Munis continue to enter rich territory as the muni-Treasury ratios continue to fall as the muni market continues to rally following suit of other fixed income products,” said Jason Wong, vice president of municipals at AmeriVet Securities.

Since the start of the rally on Nov. 1, 10-year ratios “have fallen by 15.65 percentage points, pushing us to just above the 52-week low of 59.61% which was reached on April 17,” he said.

The two-year muni-to-Treasury ratio Monday was at 57%, the three-year at 58%, the five-year at 59%, the 10-year at 59% and the 30-year at 87%, according to Refinitiv Municipal Market Data’s 3 p.m., ET, read. ICE Data Services had the two-year at 58%, the three-year at 58%, the five-year at 58%, the 10-year at 61% and the 30-year at 87% at 4 p.m.

“This rally only took us 44 days to reach our highs to just above our 52-week low signaling that many buyers are ignoring ratios and relative value and focusing solely on yields,” Wong said.

Given the historically rich ratios and after-tax spreads, Birch Creek strategists noted munis underperformed Treasuries by 12 to 17 basis points across the curve.

Investors pulled $524 million from muni mutual funds after $144 million of outflows the week prior, according to LSEG Lipper.

However, Birch Creek strategists said fund flows turned positive after the Fed announcement and will likely be supportive as investors chase after performance.

“Once we turn the page to the new year, flows may see a large ramp up as

With fears of further hikes over, Birch Creek strategists said “loads of cash still sitting on the sidelines, and expectations that cash will no longer earn 5%+, we believe the muni market will benefit in 2024 from a return of investors looking to allocate to the asset class.”

However, “with valuations already at aggressive levels, it’s hard to see how munis can outperform much from here,” they said.

Investors are likely to instead see the asset class as a “low-risk way” to earn a “respectable” tax-adjusted return, they added.

Secondary trading

California 5s of 2024 at 2.70% versus 2.96% on 12/11. Howard County, Maryland, 5s of 2025 at 2.69%. Washington 5s of 2026 at 2.56%-2.54%.

Massachusetts State Development Finance Agency 5s of 2027 at 2.27% versus 2.44%-2.41% on 12/8. NYC 5s of 2029 at 2.44%-2.40%. Connecticut 5s of 2030 at 2.45%.

Connecticut 5s of 2032 at 2.48%. California 5s of 2034 at 2.41% versus 2.64% Tuesday. Baltimore County, Maryland, 5s of 2036 at 2.55%-2.54%.

Northwest ISD, Texas, 5s of 2044 at 3.47% versus 3.68% original on Thursday. NY State Urban Development Corp. 5s of 2048 at 3.67% versus 3.90% on 12/5.

AAA scales

Refinitiv MMD’s scale was unchanged: The one-year was at 2.71% and 2.56% in two years. The five-year was at 2.31%, the 10-year at 2.33% and the 30-year at 3.53% at 3 p.m.

The ICE AAA yield curve was bumped up to two basis points: 2.75% (unch) in 2024 and 2.59% (unch) in 2025. The five-year was at 2.30% (unch), the 10-year was at 2.36% (-1) and the 30-year was at 3.51% (-1) at 4 p.m.

The S&P Global Market Intelligence municipal curve was unchanged: The one-year was at 2.71% in 2024 and 2.58% in 2025. The five-year was at 2.37%, the 10-year was at 2.47% and the 30-year yield was at 3.48%, according to a 3 p.m. read.

Bloomberg BVAL was unchanged: 2.60% in 2024 and 2.52% in 2025. The five-year at 2.24%, the 10-year at 2.32% and the 30-year at 3.41% at 4 p.m.

Treasuries were weaker.

The two-year UST was yielding 4.456% (+1), the three-year was at 4.152% (+3), the five-year at 3.942% (+3), the 10-year at 3.945% (+4), the 20-year at 4.234% (+5) and the 30-year Treasury was yielding 4.058% (+5) near the close.

Primary to come

The California Public Finance Authority (Aa3/AA//) is set to price Tuesday