Munis focus on primary, ignore UST rally

6 min read

The focus was on the primary market Wednesday as the New York City Transitional Finance Authority’s $1 billion deal saw good reception, repricing to lower yields, though municipals underperformed a U.S. Treasury rally. Equities ended in the black .

Triple-A yields fell or rose a basis point or two, depending on the scale, while Treasuries made large gains with yields falling up to 14 basis point out long.

Municipal to UST ratios rose as a result. The two-year muni-to-Treasury ratio Wednesday was at 64%, the three-year at 66%, the five-year at 67%, the 10-year at 70% and the 30-year at 91%, according to Refinitiv MMD’s 3 p.m. read. ICE Data Services had the two-year at 64%, the three-year at 65%, the five-year at 64%, the 10-year at 66% and the 30-year at 88% at 4 p.m.

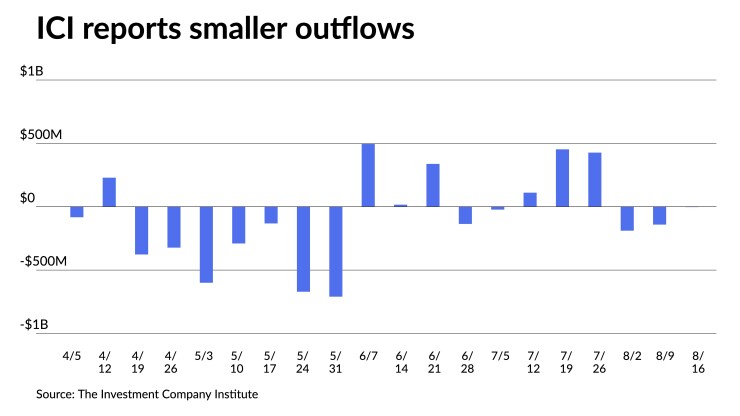

The Investment Company Institute reported investors pulled $3 million from municipal bond mutual funds in the week ending Aug. 16, after $141 million of outflows the previous week. ETFs saw outflows of $168 million after $500 million of inflows the week prior.

Despite the Treasury rally today, seasonal pressure in the municipal market continues this week as yields have risen amid Treasury weakness..

Despite the volatility and the absence of market participants, new deals are being snapped up by buyers looking for yield, experts said.

Others said the municipal market is holding its own despite the recent Treasury volatility and the decrease in trailing inflation to 3.2% from 7.7% last year at the same time.

“This is reflected in good demand for issues and the fact that the hemorrhaging of bond funds we saw last fall when Treasuries rose in yield is not happening,” John Mousseau, president and chief executive officer at Cumberland Advisors, said of the overall improving backdrop.

In the primary market Wednesday, Wells Fargo Bank priced and repriced for the New York City Transitional Finance Authority (Aa1/AAA/AAA/) is set to price Wednesday $1 billion of future tax-secured subordinate bonds, Fiscal 2024 Series B, with yields bumped up to five basis points from the preliminary pricing wire: 5s of 5/2025 at 3.20% (-3), 5s of 2028 at 3.08% (-4), 5s of 2033 at 3.29% (-3), 5s of 2038 at 3.80% (-4), 5s of 2043 at 4.18% (unch), 5s of 2048 at 4.35% (-2) and 4.375s of 2053 at 4.60% (-5), callable 11/1/2033.

Siebert Williams Shank & Co. priced and repriced for the Dormitory Authority of the State of New York (Aa3//A+/) an upsized deal of $352.205 million of State University of New York dormitory facilities revenue bonds, Series 2023, with yields bumped up to five basis points. The first tranche, $113.510 million of sustainability bonds, Series 2023A, saw 5s of 7/2024 at 3.37% (-4), 5s of 2028 at 3.15% (-3), 5s of 2033 at 3.34% (-4), 5s of 2038 at 3.86% (-6), 5s of 2043 at 4.24% (unch), 5s of 2048 at 4.40% (-5) and 5s of 2053 at 4.48% (-5), callable 7/1/2033.

The second tranche, $238.695 million of tender bonds, Series 2023B, saw 5s of 7/2024 at 3.37% (-4), 5s of 2028 at 3.15% (-3), 5s of 2033 at 3.34% (-4), 5s of 2039 at 3.96% (-3), 5s of 2043 at 4.24% (unch) and 5s of 2046 at 4.38% (unch), callable 7/1/2033.

These deals follow Tuesday’s Michigan (Aa2/AA+//) $1.194 billion of Rebuilding Michigan Program state trunk line fund bonds, Series 2023, which saw large bumps on the front end of the curve and cuts out long: 5s of 11/2024 at 3.28% (-7), 5s of 2028 at 3.03% (-8), 5s of 2033 at 3.26% (unch), 5s of 2038 at 3.74% (-2), 5s of 2043 at 4.15% (+3), 5.25s of 2049 at 4.34% (+3) and 5s of 2049 at 4.29%, callable 11/1/5/2033.

Supply scarcity is helping the market through the Treasury volatility — Bond Buyer 30-day visible supply currently sits at $4.72 billion.

Secondary trading

Ohio 5s of 2024 at 3.34%. Washington 5s of 2024 at 3.33% versus 3.36% Tuesday. LA DWP 5s of 2025 at 3.17%-3.24%.

Massachusetts 5s of 2028 at 2.94%. Ohio 5s of 2028 at 3.10%. California 5s of 2029 at 2.90% versus 2.72% on 8/16.

University of California 5s of 2032 at 2.79%-2.78% versus 2.77%-2.76% Tuesday. Energy Northwest, Washington, 5s of 2032 at 3.06%. California 5s of 2034 at 2.96%-2.94% versus 2.98% Monday and 2.79%-2.81% on 8/15.

California 5s of 2052 at 3.94%-3.81% versus 3.93% Friday. Indiana Finance Authority 5s of 2053 at 4.38% versus 4.27% on 8/16 and 4.22%-4.20% on 8/10.

AAA scales

Refinitiv MMD’s scale was bumped at one-year: The one-year was at 3.27% (-2) and 3.19% (unch) in two years. The five-year was at 2.93% (unch), the 10-year at 2.95% (unch) and the 30-year at 3.91% (unch) at 3 p.m.

The ICE AAA yield curve was bumped one basis point: 3.29% (-1) in 2024 and 3.24% (-1) in 2025. The five-year was at 2.91% (-1), the 10-year was at 2.87% (-1) and the 30-year was at 3.89% (-1) at 4 p.m.

The S&P Global Market Intelligence (formerly IHS Markit) municipal curve was cut up to three basis points: 3.29% (unch) in 2024 and 3.19% (+1) in 2025. The five-year was at 2.94% (+2), the 10-year was at 2.96% (+3) and the 30-year yield was at 3.90% (+3), according to a 4 p.m. read.

Bloomberg BVAL was bumped up to one basis point: 3.27% (-1) in 2024 and 3.18% (-1) in 2025. The five-year at 2.89% (unch), the 10-year at 2.88% (unch) and the 30-year at 3.87% (unch) at 4 p.m.

Treasuries rallied.

The two-year UST was yielding 4.959% (-8), the three-year was at 4.649% (-10), the five-year at 4.358% (-12), the 10-year at 4.187% (-14), the 20-year at 4.480% (-13) and the 30-year Treasury was yielding 4.266% (-14) at the close.

Bank downgrades and munis

Following S&P Global Ratings’ downgrades of five U.S. regional banks on Monday, participants considered what effect, if any, they may have on the muni market.

S&P downgraded the banks — KeyCorp, Comerica Inc., Valley National Bancorp, UMB Financial Corp. and Associated Banc-Corp. — by one notch and signaled a negative outlook for several others on Monday.

The ratings agency blamed the current “tough” lending environment for the downgrade action, which followed similar downgrades by Moody’s Investors Service two weeks prior.

While some said the downgrade activity would not affect the municipal market, others said it could have a trickle-down to higher transactional costs and wider spreads going forward.

“Downgrade actions on financial institutions could have implications for the municipal bond market to the extent where certain securities and structures are backed by such institutions,” Jeff Lipton, head of municipal credit and market strategy and municipal capital markets at Oppenheimer & Co. said on Wednesday.

For instance, he said the ratings on a number of variable rate demand obligations could be downgraded given correlation to the assignment of a direct pay letter of credit or to a liquidity facility provided by a particular banking enterprise.

“Multiple downgrades on these entities could narrow the universe of available short-term support providers, which could result in higher transactional costs to the issuer community,” Lipton said.

Other types of structures, such as prepay gas bonds, may see a widening in spreads, according to Lipton, even though backing for these bonds typically derives from larger, bulge-bracket national banking institutions.

“This phenomenon could create buying opportunities for sophisticated investors,” Lipton said.

But others, like Roberto Roffo, managing director and portfolio manager at SWBC Investment Company, said the S&P downgrade should have limited impact on the municipal market unless there is another similar collapse, like Silicon Valley Bank.

“The downgrades reflect the tougher environment in which the banks have to operate and an increased potential of something going wrong — but nothing imminent,” Roffo said.

Primary still to come:

The Wisconsin Housing and Economic Development Authority (Aa2/AA+//) is set to price Thursday $185 million of non-AMT home ownership revenue social bonds, serials 2024-2035, terms 2038, 2043, 2049, 2054. RBC Capital Markets.

The Ohio Housing Finance Agency (Aaa///) is set to price Thursday $145 million of non-AMT mortgage-backed securities program residential mortgage revenue social bonds, Series 2023 B, serials 2025-2035, terms 2038, 2043, 2048, 2054, 2055. Citigroup Global Markets Inc.

The California Infrastructure and Economic Development Bank (Aa2///) is set to price Thursday $113.215 million of Academy of Motion Pictures Arts and Sciences Obligated Group revenue refunding bonds, Series 2023A, serials 2024-2030, 2033-2041. Wells Fargo Bank.

The Indiana Finance Authority (Aaa/AAA/AAA/) is set to price Thursday $100 million of state revolving fund program green bonds, Series 2023B, serials 2030-2044. RBC Capital Markets.

Competitive

The Metropolitan School District of the Washington Township School Building Corp., Indiana (/AA+//) is set to sell $120 million of unlimited ad valorem property tax first mortgage bonds, Series 2023, at 11:30 a.m. eastern Thursday.

The Bellingham School District No. 501, Washington (Aaa///), is set to sell $109.440 million of unlimited tax general obligation and refunding bonds, at 11 a.m. Thursday.